What is a VA IRRR

If you currently have a VA home loan, you have access to one of the most powerful and efficient refinancing options in the mortgage industry. The VA Interest Rate Reduction Refinance Loan, commonly referred to as the VA IRRRL or the VA Streamline Refinance, is a specialized mortgage product designed exclusively for veterans, active duty military personnel, and eligible surviving spouses.

The primary goal of the VA IRRRL program is simple. It exists to put veterans in a better financial position by replacing their current VA loan with a new VA loan at a lower interest rate. Because this program is designed strictly for borrowers who have already been approved for a VA loan in the past, the Department of Veterans Affairs has removed many of the traditional hurdles associated with refinancing a mortgage.

At United States VA Loans, we specialize in helping veterans navigate this fast-tracked process. Whether you are looking to lower your monthly payment, reduce your interest rate, or switch from an adjustable rate mortgage to a stable fixed rate mortgage, Danny Plattner and our dedicated team are here to guide you every step of the way.

Top Benefits of the VA Streamline Refinance

The VA IRRRL is widely considered one of the most borrower-friendly mortgage products available today. When you choose to refinance your current mortgage through United States VA Loans, you unlock a variety of exclusive benefits that are not available with conventional or FHA home loans.

1. Lower Interest Rates and Monthly Payments

The most significant advantage of an IRRRL is the ability to secure a lower interest rate. A lower rate directly translates to a lower monthly mortgage payment, freeing up your cash flow for other financial goals. Over the life of a thirty-year mortgage, even a seemingly small reduction in your interest rate can save you tens of thousands of dollars in interest charges.

2. No Appraisal Required

Traditional refinancing usually requires a new home appraisal to verify the current market value of your property. The VA IRRRL program generally waives this requirement. This means you do not have to pay out of pocket for an appraisal fee. Furthermore, if your home has temporarily decreased in value, you can still qualify for the refinance. You can be underwater on your mortgage and still take advantage of lower interest rates.

3. No Income or Employment Verification

Because you have already proven your ability to qualify for a VA loan when you originally purchased your home, the VA does not require lenders to re-verify your income or employment for an IRRRL. You do not need to submit recent pay stubs, W-2s, or tax returns. This drastically reduces the amount of paperwork you need to gather and significantly speeds up the underwriting process.

4. Minimal Credit Checks

While lenders will pull a credit report to ensure you have been making your current mortgage payments on time, the credit requirements for an IRRRL are incredibly lenient. The VA itself does not set a minimum credit score requirement for this program. As long as you have a flawless payment history on your current VA loan over the past year, you are in an excellent position to be approved.

5. No Out-of-Pocket Closing Costs

Refinancing a home involves closing costs, but the VA IRRRL allows you to roll all of your closing costs directly into the total loan amount. You also have the option to price the loan so that the lender covers the closing costs in exchange for a slightly higher interest rate. This means you can successfully refinance your home and lower your payment without bringing a single dollar to the closing table.

6. Switch from an ARM to a Fixed-Rate Mortgage

If you currently have an Adjustable Rate Mortgage (ARM) and want the long-term stability of a fixed monthly payment, the IRRRL is the perfect solution. The VA allows you to use this program to convert your unpredictable ARM into a secure fixed rate loan, protecting you from future interest rate hikes.

Eligibility Requirements for a VA IRRRL

While the VA Streamline Refinance is designed to be as accessible as possible, there are specific guidelines set by the Department of Veterans Affairs that you must meet to qualify. Danny Plattner and the team at United States VA Loans will help you verify your eligibility quickly and accurately.

- Existing VA Loan: You must currently have a VA-backed home loan. You cannot use an IRRRL to refinance a conventional loan, an FHA loan, or a USDA loan. If you have a non-VA loan and want to switch to a VA loan, you will need to apply for a VA Cash-Out Refinance instead.

- Prior Occupancy: Unlike VA purchase loans which require you to currently live in the home as your primary residence, the IRRRL only requires you to certify that you previously occupied the home. This is incredibly beneficial for military personnel who have received Permanent Change of Station (PCS) orders and are currently renting out their former primary residence.

- Flawless Payment History: You must be current on your existing mortgage. Generally, you cannot have had any late payments of 30 days or more within the last 12 months. If you have had your loan for less than 12 months, you must have made all payments on time since the loan originated.

- Seasoning Requirements: The VA requires a specific waiting period before you can refinance. You must wait until you have made at least six consecutive monthly payments on your current VA loan, and at least 210 days must have passed since your first payment was due.

- Net Tangible Benefit: The VA requires lenders to prove that the refinance is strictly in your best financial interest. This is known as the Net Tangible Benefit rule.

Understanding the Net Tangible Benefit (NTB) Rule

To protect veterans from predatory lending practices, the VA enforces strict rules regarding the financial advantage of an IRRRL. To be approved, your new loan must meet specific criteria:

- If you are refinancing from a fixed rate loan to a new fixed rate loan, your new interest rate must be at least 0.5% lower than your current interest rate.

- If you are refinancing from a fixed rate loan to an adjustable rate mortgage (ARM), your new interest rate must be at least 2.0% lower than your current rate.

- The time it takes to recoup the closing costs and fees associated with the refinance (the break-even point) cannot exceed 36 months. This calculation strictly uses the monthly savings generated by the lower interest rate and lower principal payment.

There is one major exception to the interest rate reduction rule. If you are using the IRRRL to switch from an ARM to a fixed rate mortgage, the VA does not require your new interest rate to be lower. Gaining the stability of a fixed rate is considered a sufficient Net Tangible Benefit on its own.

How the VA IRRRL Process Works

Refinancing your home should not be a stressful or overly complicated endeavor. At United States VA Loans, we have optimized our workflow to ensure your VA Streamline Refinance is handled with speed, precision, and complete transparency. Here is a step-by-step look at what you can expect when you work with Danny Plattner.

Step 1: The Initial Consultation

The process begins with a simple phone call or email. You can reach Danny Plattner directly at 520-241-1428 or via email at unitedstatesvaloans@gmail.com. During this initial conversation, we will review your current mortgage statement, discuss your financial goals, and determine if an IRRRL makes sense for your unique situation.

Step 2: Securing Your Certificate of Eligibility (COE)

Because you already have a VA loan, obtaining your Certificate of Eligibility is usually an automated process. Our team can typically pull your COE directly from the VA portal in a matter of minutes. You do not need to spend time hunting down old military paperwork or discharge documents.

Step 3: Locking in Your Lower Interest Rate

Once we have verified your eligibility and confirmed that the new loan meets the Net Tangible Benefit requirements, we will present you with your new interest rate and monthly payment options. When you are ready, we will lock in your rate to protect you from any sudden market fluctuations.

Step 4: Streamlined Underwriting

Because there is no appraisal required and no income verification needed, the underwriting phase for an IRRRL is incredibly fast. Our processing team will prepare your streamlined loan file, verify your mortgage payment history, and submit the file for final approval. Our goal is to make this phase entirely hands-off for you.

Step 5: Closing Your Loan

Once your loan is cleared to close, we will schedule a convenient time for you to sign your final documents. You can often complete your closing from the comfort of your own home using a mobile notary. After a mandatory three-day waiting period, your new loan will fund, your old loan will be paid off, and you will officially start enjoying your lower monthly payments.

VA IRRRL Costs and Fees

While the VA IRRRL eliminates many of the traditional costs associated with refinancing, there are still some fees involved. It is crucial to understand these costs so you can make an informed financial decision.

The VA Funding Fee

The Department of Veterans Affairs charges a mandatory funding fee on almost all VA loans. This fee goes directly to the VA to help keep the home loan program running for future generations of veterans. For a VA IRRRL, the funding fee is significantly reduced compared to purchase loans.

The funding fee for a VA IRRRL is exactly 0.5% of the total loan amount. For example, if you are refinancing a loan balance of $300,000, the VA funding fee would be $1,500.

Funding Fee Exemptions

Many veterans do not have to pay the VA funding fee at all. You are completely exempt from paying the 0.5% fee if you meet any of the following criteria:

- You are receiving VA compensation for a service-connected disability.

- You are entitled to receive VA compensation for a service-connected disability, but you are currently receiving retirement or active duty pay instead.

- You are the surviving spouse of a veteran who died in service or from a service-connected disability.

- You are an active duty service member who has been awarded the Purple Heart.

Standard Closing Costs

In addition to the VA funding fee, you will encounter standard mortgage closing costs. These typically include title search fees, title insurance, recording fees, and lender origination fees. As mentioned earlier, all of these costs can be rolled into your new loan balance, ensuring you do not have to empty your savings account to secure a lower interest rate.

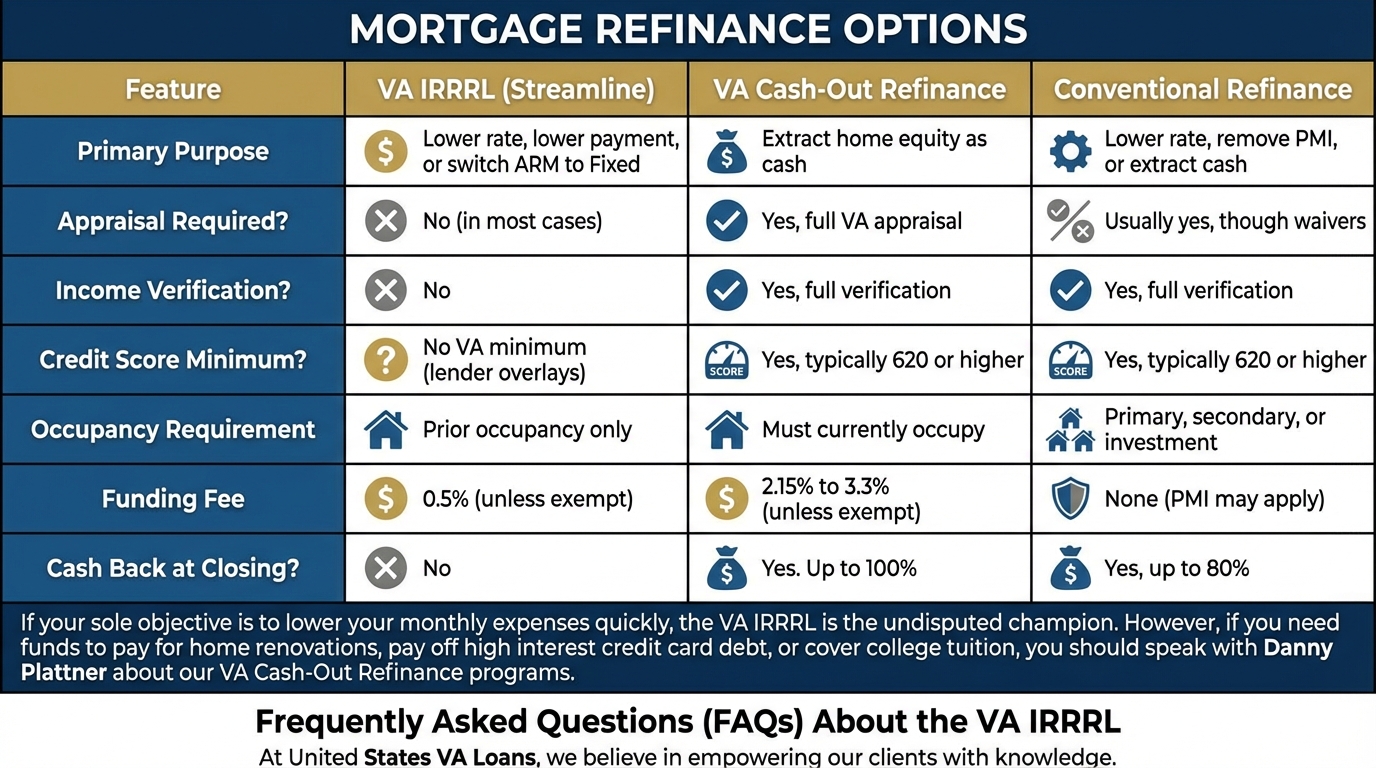

Comparing Refinance Options: IRRRL vs. Cash-Out vs. Conventional

Comparison of Mortgage Refinance OptionsFeatureVA IRRRL (Streamline)VA Cash-Out RefinanceConventional RefinancePrimary PurposeLower rate, lower payment, or switch ARM to Fixed.Extract home equity as cash, consolidate debt.Lower rate, remove mortgage insurance, or extract cash.Appraisal Required?No (in most cases).Yes, a full VA appraisal is required.Usually yes, though waivers sometimes apply.Income Verification?No.Yes, full verification required.Yes, full verification required.Credit Score Minimum?No VA minimum (lender overlays may apply, but very lenient).Yes, typically 620 or higher.Yes, typically 620 or higher.Occupancy RequirementPrior occupancy only.Must currently occupy as primary residence.Primary, secondary, or investment properties allowed.Funding Fee0.5% (unless exempt).2.15% to 3.3% (unless exempt).None, but private mortgage insurance (PMI) may apply.Cash Back at Closing?No. Strictly limited to minor reimbursement of overages.Yes. Up to 100% of the home's value in some cases.Yes, up to 80% of the home's value typically.

Comparison of Mortgage Refinance OptionsFeatureVA IRRRL (Streamline)VA Cash-Out RefinanceConventional RefinancePrimary PurposeLower rate, lower payment, or switch ARM to Fixed.Extract home equity as cash, consolidate debt.Lower rate, remove mortgage insurance, or extract cash.Appraisal Required?No (in most cases).Yes, a full VA appraisal is required.Usually yes, though waivers sometimes apply.Income Verification?No.Yes, full verification required.Yes, full verification required.Credit Score Minimum?No VA minimum (lender overlays may apply, but very lenient).Yes, typically 620 or higher.Yes, typically 620 or higher.Occupancy RequirementPrior occupancy only.Must currently occupy as primary residence.Primary, secondary, or investment properties allowed.Funding Fee0.5% (unless exempt).2.15% to 3.3% (unless exempt).None, but private mortgage insurance (PMI) may apply.Cash Back at Closing?No. Strictly limited to minor reimbursement of overages.Yes. Up to 100% of the home's value in some cases.Yes, up to 80% of the home's value typically.

If your sole objective is to lower your monthly expenses quickly and with minimal paperwork, the VA IRRRL is the undisputed champion. However, if you need funds to pay for home renovations, pay off high interest credit card debt, or cover college tuition, you should speak with Danny Plattner about our VA Cash-Out Refinance programs.

Frequently Asked Questions (FAQs) About the VA IRRRL

At United States VA Loans, we believe in empowering our clients with knowledge. Below are some of the most common questions we receive from veterans regarding the VA Streamline Refinance program.

Can I get cash out with a VA IRRRL?

Can I use an IRRRL for an investment property?

Yes, under specific conditions. You can use the IRRRL program to refinance a property that is currently an investment property or a second home, provided that you can certify you previously occupied the home as your primary residence. This is a massive benefit for veterans who purchased a home, lived in it, and later relocated while keeping the original property as a rental.

What if my home has lost value or I am underwater on my mortgage?

Do I need to find my Certificate of Eligibility (COE) again?

In the vast majority of cases, no. Because you already have a VA loan, your eligibility has already been established in the VA system. Our team at United States VA Loans can typically pull your COE electronically using our direct access to the VA portal. You will not need to track down your DD-214 unless there is a specific discrepancy in the system.

How many times can I use the VA IRRRL program?

There is no legal limit to how many times you can use the VA IRRRL program over the course of your life. However, every time you refinance, you must meet the strict Net Tangible Benefit rules and the seasoning requirements. You must wait at least 210 days and make six consecutive payments between refinances, and the new loan must mathematically improve your financial situation according to VA guidelines.

What is the maximum loan amount for an IRRRL?

The maximum loan amount for an IRRRL is determined by your current outstanding principal balance, plus any allowable closing costs, lender fees, energy efficiency improvements, and the VA funding fee. You cannot arbitrarily increase the loan amount beyond what is necessary to pay off the existing loan and cover the costs of the transaction.

Can I add or remove a borrower from the mortgage?

The VA IRRRL rules regarding changes to the borrowers on the loan are strict. Generally, the borrowers on the new loan must be the exact same as the borrowers on the original loan. However, there are exceptions. You can remove a spouse from the loan if you have gone through a divorce, or you can add a new spouse to the loan if you have recently married. You cannot, however, add a non-spouse to the loan, nor can you remove a veteran from the loan while keeping a non-veteran on the mortgage.

Can I shorten the term of my mortgage with an IRRRL?

Yes. You can use an IRRRL to refinance from a 30-year mortgage to a 15-year mortgage. However, doing so will likely increase your monthly payment, even if your interest rate drops significantly. If your payment increases by 20% or more, the VA requires the lender to perform a full credit and income qualification to ensure you can comfortably afford the higher monthly obligation.

Are there any energy efficiency improvements I can include?

Yes. The VA allows you to roll up to $6,000 in approved Energy Efficient Mortgage (EEM) improvements into your IRRRL. This can be used for upgrades such as solar heating systems, insulation, storm windows, and programmable thermostats. Adding these costs will increase your loan balance, but the energy savings are designed to offset the slightly higher mortgage payment.

Why Choose United States VA Loans for Your IRRRL?

Refinancing a home is a major financial decision. You deserve to work with a team that respects your service, understands the intricacies of VA lending guidelines, and prioritizes your long-term financial health.

Danny Plattner and the professionals at United States VA Loans have dedicated their careers to serving veterans across the nation. While our roots are tied to the 520 area code, our reach extends across the United States. We are not a generic call center. When you reach out to us, you get personalized, expert advice tailored to your specific family needs.

- Veteran-Focused Expertise: We specialize in VA loans. We know the VA manual inside and out, ensuring your loan is structured perfectly to avoid delays.

- Transparent Pricing: We believe in honest, upfront communication. We will break down every fee, explain your interest rate options, and show you exactly how long it will take to break even on your refinance.

- Speed and Efficiency: We leverage the latest mortgage technology to streamline the paperwork process. Our goal is to get you from application to closing in record time.

- Unmatched Customer Service: You will have a dedicated point of contact throughout the entire process. Danny Plattner is always just a phone call or an email away.

Contact Us Today to Start Your VA Streamline Refinance

If you are ready to take advantage of lower interest rates and reduce your monthly mortgage payment, do not wait. Mortgage rates fluctuate daily, and locking in your rate now can save you thousands of dollars over the life of your loan.

Reach out to Danny Plattner and the team at United States VA Loans today for a free, no-obligation IRRRL rate quote and savings analysis.

- Contact Name: Danny Plattner

- Phone Number: 520-241-1428

- Email Address: unitedstatesvaloans@gmail.com

- Website: www.UnitedStatesVAloans.com

Thank you for your service to our country. We look forward to serving you and helping you achieve your financial goals through the VA IRRRL program.

Compliance & Legal Disclaimer: The information provided on this page is for educational purposes only and does not constitute financial or legal advice. United States VA Loans is a private mortgage lending entity and is not affiliated with the Department of Veterans Affairs (VA) or any government agency. All loan approvals are subject to credit, income, and property qualifications. Interest rates and program guidelines are subject to change without notice. Please consult with a licensed loan originator to discuss your specific financial situation.

© 2023 United States VA Loans. All Rights Reserved.

About Us