VA Cash Out Refinance Loans

Ultimate Guide to VA Cash Out Refinance Loans

If you are a veteran, active duty service member, or eligible surviving spouse, you have access to one of the most powerful home financing tools available in the mortgage market today. At United States VA Loans, we specialize in helping our nations heroes leverage their hard-earned home equity through a VA Cash Out Refinance. Whether you want to consolidate high-interest debt, fund major home improvements, or secure a financial safety net, a VA Cash Out loan offers unparalleled benefits and flexibility.

Led by mortgage expert Danny Plattner, our team is dedicated to providing clear, honest, and transparent guidance. We understand that navigating the mortgage process can be overwhelming. That is why we have created this comprehensive guide to help you understand every aspect of the VA Cash Out Refinance program. If you are ready to explore your options, contact Danny Plattner directly at 5202411428 or email unitedstatesvaloans@gmail.com.

What is a VA Cash Out Refinance?

A VA Cash Out Refinance is a mortgage loan guaranteed by the Department of Veterans Affairs that allows eligible homeowners to refinance their current mortgage and extract cash from their accumulated home equity. Unlike the VA Interest Rate Reduction Refinance Loan (IRRRL), which is strictly for lowering your interest rate or changing your loan term, the cash out option allows you to turn your homes equity into liquid cash.

One of the most significant advantages of the VA Cash Out program is that it allows qualified borrowers to finance up to 100 percent of their homes appraised value. Conventional and FHA cash out refinances typically cap your borrowing power at 80 percent of the homes value. This unique 100 percent loan-to-value (LTV) allowance makes the VA Cash Out Refinance an incredibly potent financial tool for veterans.

It is also important to note that you do not need to currently have a VA loan to utilize a VA Cash Out Refinance. If you purchased your home using a conventional loan, an FHA loan, or a USDA loan, you can refinance that existing mortgage into a VA loan and pull cash out, provided you meet the VA eligibility requirements.

Why Choose United States VA Loans for Your Refinance?

When it comes to your home and your financial future, working with a knowledgeable and trustworthy mortgage lender is critical. United States VA Loans is committed to serving those who have served our country. Here is why veterans across the nation choose to work with us:

- Veteran-Focused Expertise: We specialize in VA loans. We understand the nuances of the Certificate of Eligibility (COE), VA funding fees, and VA appraisal requirements better than generalized lenders.

- Personalized Service: You are not just a number in a corporate queue. Danny Plattner and our team provide one-on-one consultations to ensure your loan aligns with your long-term financial goals.

- Competitive Rates: We work tirelessly to secure the most competitive interest rates available for your VA Cash Out Refinance, keeping your monthly payments as low as possible.

- Streamlined Process: We utilize the latest technology and our deep industry knowledge to move your loan from application to closing quickly and efficiently.

Ready to see how much cash you can access?

Visit us at www.UnitedStatesVAloans.com or call 5202411428 to start your free, no-obligation consultation.

Key Benefits of a VA Cash Out Refinance

The VA Cash Out Refinance program is packed with benefits designed specifically to reward your military service. Understanding these advantages will help you make an informed decision about your home equity.

Up to 100 Percent Loan-to-Value (LTV)

As mentioned earlier, the ability to access up to 100 percent of your homes equity is a game-changer. For example, if your home appraises for $400,000 and you currently owe $250,000, you potentially have access to up to $150,000 in equity (minus closing costs and fees). Most other loan types would restrict your maximum new loan to $320,000, severely limiting your cash access.

No Private Mortgage Insurance (PMI) Required

In the conventional mortgage world, borrowing more than 80 percent of your homes value triggers a requirement for Private Mortgage Insurance (PMI). This insurance protects the lender, not you, and adds a significant monthly expense to your mortgage payment. The VA guarantees a portion of the loan, completely eliminating the need for PMI, regardless of how much equity you extract.

Lower Interest Rates

Because the Department of Veterans Affairs backs these loans, lenders assume less risk. This reduced risk translates directly into lower interest rates for you. VA loans historically offer lower average interest rates than both conventional and FHA mortgages.

Flexible Credit Requirements

The VA does not set a strict minimum credit score requirement for a VA Cash Out Refinance. While individual lenders (including United States VA Loans) will have their own minimum overlays to ensure responsible lending, the credit requirements are generally much more forgiving than those for conventional loans. This makes it easier for veterans who have experienced financial bumps in the road to secure approval.

Ability to Refinance Non-VA Loans

If you bought your home before you were eligible for a VA loan, or if you simply chose a different loan type at the time of purchase, you are not locked out of VA benefits. You can refinance an existing conventional, FHA, or USDA loan into a VA loan, allowing you to drop PMI, lower your rate, and pull cash out simultaneously.

How Veterans Use VA Cash Out Funds

Once your VA Cash Out Refinance is funded, there are no restrictions on how you can use the money. The cash is yours to spend as you see fit. However, our experts at United States VA Loans highly recommend using these funds for activities that improve your overall financial health. Here are the most common and beneficial ways veterans utilize their cash out funds.

High-Interest Debt Consolidation

This is arguably the most popular and financially sound use of a VA Cash Out Refinance. Credit cards, personal loans, and auto loans typically carry much higher interest rates than a mortgage. By paying off these debts with the proceeds from your VA loan, you consolidate multiple high payments into one single, lower-interest monthly mortgage payment. This can free up hundreds or even thousands of dollars in your monthly budget, drastically improving your cash flow.

Home Improvements and Renovations

Reinvesting your equity back into your home is a smart way to build long-term wealth. Whether you are updating a dated kitchen, adding a new bathroom, replacing an aging roof, or building an addition to accommodate a growing family, using a VA Cash Out Refinance provides the necessary capital. Unlike a construction loan or a high-interest personal loan, the VA loan offers a low, fixed rate spread out over 15 to 30 years.

Funding Higher Education

College tuition and living expenses are rising rapidly. While the GI Bill provides incredible educational benefits, it may not cover everything, especially if you have children heading to college. A VA Cash Out Refinance can provide the funds needed to pay for tuition without resorting to high-interest private student loans.

Creating an Emergency Safety Net

Life is unpredictable. Medical emergencies, sudden job losses, or major unexpected expenses can derail a family's financial stability. Extracting cash from your home equity to build a robust savings account can provide peace of mind and protect your family from future financial shocks.

Purchasing Investment Properties

Some savvy veterans use their primary residence equity to generate more income. You can use the cash out proceeds as a down payment on a secondary home, a vacation rental, or a multi-family investment property. This strategy allows you to leverage your existing assets to build a diversified real estate portfolio.

Comparing Your Options: VA Cash Out vs. Other Equity Solutions

To fully understand the value of a VA Cash Out Refinance, it is helpful to compare it to other common methods of accessing home equity. Below is a detailed comparison table outlining the differences between a VA Cash Out Refinance, a Conventional Cash Out Refinance, and a Home Equity Line of Credit (HELOC).

Feature

VA Cash Out Refinance

Conventional Cash Out

HELOC (Home Equity Line of Credit)

Maximum Loan-to-Value (LTV)

Up to 100 percent

Typically capped at 80 percent

Usually capped at 80 to 85 percent

Mortgage Insurance (PMI)

None required

Required if LTV exceeds 80 percent

Not typically required, but rates are higher

Interest Rate Type

Fixed (usually)

Fixed (usually)

Variable (fluctuates with prime rate)

Credit Score Requirements

Flexible (Lender specific)

Strict (Usually 620 or higher)

Strict (Usually 680 or higher)

Loan Structure

Replaces existing first mortgage

Replaces existing first mortgage

Acts as a second mortgage

Funding Fee

Yes (VA Funding Fee applies)

No, but closing costs apply

Minimal closing costs, sometimes zero

If you are unsure which option is best for your specific scenario, Danny Plattner and the team at United States VA Loans are here to help. Give us a call at 5202411428 for a personalized financial review.

Eligibility Requirements for a VA Cash Out Loan

To take advantage of the VA Cash Out Refinance program, you must meet both the Department of Veterans Affairs eligibility standards and the specific underwriting guidelines of your lender. Here is a detailed breakdown of what is required.

Service Requirements and the Certificate of Eligibility (COE)

The foundational requirement for any VA loan is proving your military service. You must obtain a Certificate of Eligibility (COE). You may be eligible if you meet one of the following criteria:

- You served 90 consecutive days of active service during wartime.

- You served 181 days of active service during peacetime.

- You have 6 years of service in the National Guard or Reserves.

- You are the surviving spouse of a service member who died in the line of duty or as a result of a service-connected disability.

If you do not have your COE handy, do not worry. When you work with United States VA Loans, we can often pull your COE electronically in a matter of minutes through the VA approved lender portal.

Credit Score and History

While the VA itself does not mandate a minimum credit score, lenders assume the financial risk of issuing the loan. Therefore, lenders apply their own credit minimums, known as overlays. A credit score of 620 is a common benchmark, though some lenders may accept lower scores with compensating factors. Underwriters will also review your credit history for recent bankruptcies, foreclosures, or a pattern of late payments.

Income and Employment Verification

You must prove that you have stable, reliable income sufficient to cover the new mortgage payment along with your other monthly debts. We will review your W-2s, recent pay stubs, and tax returns. The VA focuses heavily on your Debt-to-Income (DTI) ratio and your residual income. Residual income is the amount of money you have left over each month after paying your major expenses. The VA uses residual income guidelines to ensure veterans have enough money to cover basic living expenses like food, transportation, and family care.

Occupancy Requirements

VA loans are designed to help veterans purchase and maintain primary residences. You cannot use a VA Cash Out Refinance on an investment property or a vacation home. You must certify that you intend to occupy the home as your primary residence.

The VA Cash Out Refinance Process: Step by Step

At United States VA Loans, we believe in total transparency. Knowing what to expect can alleviate the stress often associated with mortgage refinancing. Here is the step-by-step journey of securing your VA Cash Out Refinance with Danny Plattner.

Step 1: Initial Consultation and Goal Setting

Your journey begins with a simple phone call to 5202411428 or an email to unitedstatesvaloans@gmail.com. During this initial conversation, we will discuss your financial goals. Are you looking to pay off credit cards? Remodel your kitchen? We will evaluate your current mortgage, estimate your homes value, and determine if a VA Cash Out Refinance makes mathematical sense for you.

Step 2: Obtaining Your COE

If you have not already secured your Certificate of Eligibility, our team will assist you in acquiring it directly from the VA portal. This document is the key that unlocks your VA benefits.

Step 3: Completing the Loan Application

Once we have established your goals and eligibility, we will guide you through the formal loan application. You will need to provide financial documentation, including:

- Government-issued ID

- Recent pay stubs (usually covering the last 30 days)

- W-2 forms for the past two years

- Federal tax returns for the past two years

- Recent bank statements

- Current mortgage statement and homeowners insurance declaration page

Step 4: The VA Appraisal

Unlike the VA IRRRL streamline refinance, a VA Cash Out Refinance absolutely requires a full home appraisal. The VA appraisal serves two purposes. First, it determines the current fair market value of your home, which dictates how much cash you can extract. Second, the appraiser ensures the property meets the VAs Minimum Property Requirements (MPRs). The home must be safe, structurally sound, and sanitary.

Step 5: Processing and Underwriting

While the appraisal is being conducted, our processing team will verify all your documentation. The file is then sent to an underwriter. The underwriter is the person who reviews your credit, income, and the appraisal to ensure the loan meets all VA and lender guidelines. They may ask for additional letters of explanation or updated documents during this phase.

Step 6: Closing and Funding

Once the underwriter issues a Clear to Close, we will schedule your closing appointment. You will sign the final loan documents, which can often be done with a mobile notary at your home or office. By federal law, cash out refinances on primary residences are subject to a three-day right of rescission. This means you have three business days after signing to cancel the loan if you change your mind. Once this waiting period expires, your old loan is paid off, and your cash out funds are wired directly to your bank account.

Understanding the VA Funding Fee for Cash Out Refinances

For a VA Cash Out Refinance, the funding fee is calculated as a percentage of the total loan amount. The percentage depends on whether this is your first time using your VA loan benefit or if you have used it previously.

- First-Time Use: If you are using your VA loan benefit for the very first time on a cash out refinance, the funding fee is typically 2.15 percent of the loan amount.

- Subsequent Use: If you have used a VA loan before, the funding fee for a cash out refinance increases to 3.3 percent of the loan amount.

Important Note on Paying the Fee: You do not have to pay this fee out of your own pocket at closing. The vast majority of veterans choose to roll the VA Funding Fee into the total loan amount, financing it over the life of the loan.

VA Funding Fee Exemptions

Many veterans are entirely exempt from paying the VA Funding Fee. You will not have to pay this fee if you meet any of the following conditions:

- You are receiving VA compensation for a service-connected disability.

- You are eligible to receive VA compensation for a service-connected disability, but you are receiving retirement or active duty pay instead.

- You are the surviving spouse of a veteran who died in service or from a service-connected disability.

- You are an active duty service member who has been awarded the Purple Heart.

If you are unsure about your exemption status, Danny Plattner and the team at United States VA Loans will verify this for you during the initial setup process.

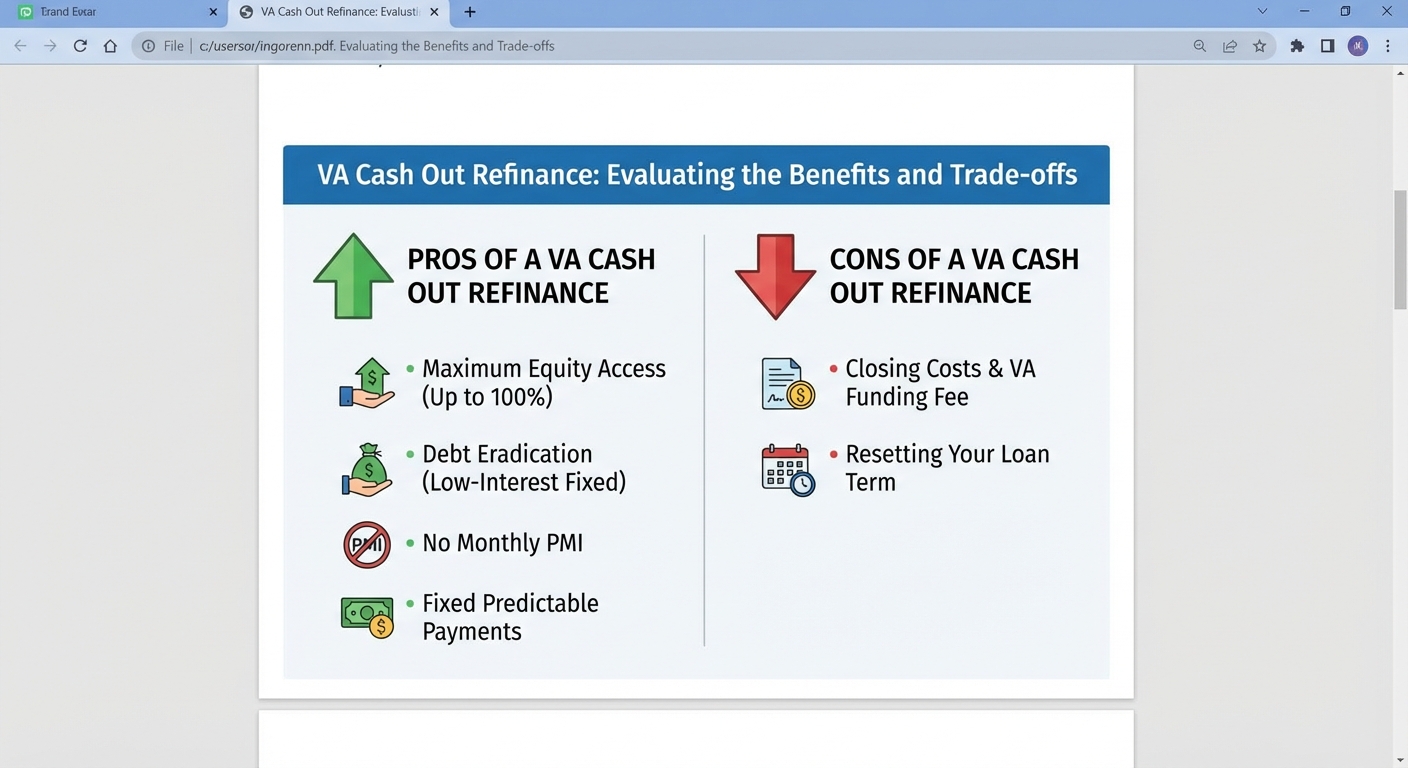

Pros and Cons of a VA Cash Out Refinance

The Pros

- Maximum Equity Access: The ability to borrow up to 100 percent of your homes value is unmatched in the mortgage industry.

- Debt Eradication: Paying off 25 percent interest credit cards with a low-interest fixed mortgage can save you thousands of dollars a year and vastly improve your monthly quality of life.

- No Monthly PMI: Keeping your monthly payments lower by avoiding Private Mortgage Insurance.

- Fixed Predictable Payments: Unlike a HELOC, which has a fluctuating interest rate, a VA Cash Out Refinance gives you a fixed rate, meaning your principal and interest payment will never change.

The Cons

- Closing Costs and Fees: Refinancing involves closing costs (title fees, appraisal fees, lender fees) and the VA Funding Fee. You must ensure the financial benefit of the refinance outweighs these costs.

- Resetting Your Loan Term: If you are 10 years into a 30-year mortgage and you refinance into a new 30-year loan, you are extending the time it will take to pay off your home. (Though you can opt for a 15-year or 20-year term to mitigate this).

- Risk of Foreclosure: When you consolidate unsecured debt (like credit cards) into your mortgage, you are converting unsecured debt into secured debt. Your home is the collateral. If you fail to make your mortgage payments, you risk losing your home.

- Less Equity for the Future: Pulling cash out means you have less equity in your home. If property values decline, you could potentially end up owing more than the home is worth (being underwater).

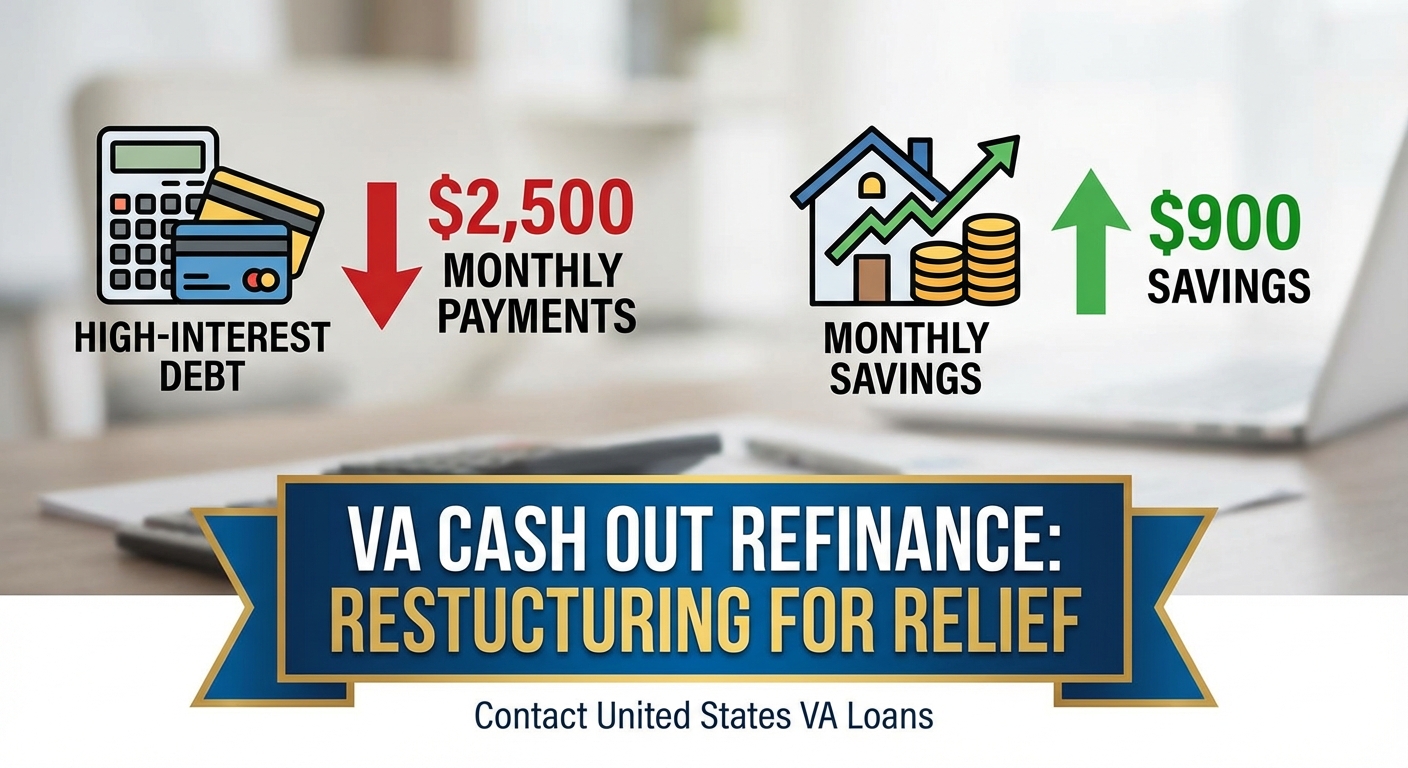

Financial Scenario: The Power of Debt Consolidation

Meet John, a veteran who owns a home valued at $350,000. Johns current VA mortgage balance is $200,000. His current mortgage payment (principal and interest) is $1,100 per month. Over the past few years, John has accumulated significant high-interest debt due to unexpected home repairs and medical bills.

Johns Current Debt Profile:

- Current Mortgage: $200,000 balance ($1,100/month payment)

- Credit Card 1: $15,000 balance at 22 percent interest ($450/month minimum payment)

- Credit Card 2: $10,000 balance at 24 percent interest ($350/month minimum payment)

- Personal Loan: $25,000 balance at 12 percent interest ($600/month payment)

Total Current Monthly Debt Payments: $2,500

John contacts Danny Plattner at United States VA Loans to explore a VA Cash Out Refinance. John wants to borrow enough to pay off his current mortgage plus all $50,000 of his consumer debt. His new loan amount will be approximately $255,000 (including closing costs and the VA funding fee).

With a new 30-year fixed VA Cash Out Refinance, Johns new mortgage payment (principal and interest) becomes approximately $1,600 per month. Because all his credit cards and personal loans are paid off at closing, he no longer has those monthly payments.

The Result:

- Old Monthly Payments: $2,500

- New Monthly Payment: $1,600

- Monthly Savings: $900

By restructuring his debt using his home equity, John frees up $900 every single month. He can use this extra cash flow to build his savings, invest for retirement, or even make extra principal payments on his new mortgage to pay it off faster.

Frequently Asked Questions (FAQs) About VA Cash Out Refinances

We receive many questions from veterans regarding the cash out process. Here are detailed answers to the most frequently asked questions we receive at United States VA Loans.

How long does a VA Cash Out Refinance take?

On average, the process takes between 30 to 45 days from the time you submit a complete application to the day your loan closes. The timeline is primarily driven by how quickly the VA appraisal can be completed and how fast you provide requested documentation to our processing team.

Can I do a VA Cash Out Refinance with bad credit?

While the VA does not dictate a minimum credit score, lenders do. If your credit score is below 620, it may be more challenging to secure approval. However, we look at the entire financial picture. If you have lower credit, we highly recommend contacting Danny Plattner at 5202411428 to discuss your specific situation. We can often provide guidance on how to quickly improve your score to qualify.

Do I have to pay taxes on the cash I receive?

No. The cash you receive from a cash out refinance is considered a loan, not income. Therefore, it is not subject to state or federal income taxes. However, it is always recommended to consult with a licensed tax professional regarding your specific financial situation and how mortgage interest deductions may apply.

Can I use a VA Cash Out Refinance to buy land or another house?

Yes. Once the loan closes, the cash is deposited into your bank account, and there are no VA restrictions on how you use the money. You can absolutely use the funds as a down payment on an investment property, a second home, or a plot of land.

What is the difference between an IRRRL and a VA Cash Out Refinance?

The VA Interest Rate Reduction Refinance Loan (IRRRL), also known as a streamline refinance, is designed solely to lower your interest rate or change your loan term (e.g., from an adjustable rate to a fixed rate). You cannot pull cash out with an IRRRL. An IRRRL generally requires less paperwork, no appraisal, and no income verification. A VA Cash Out Refinance allows you to extract equity as cash but requires a full appraisal, income verification, and comprehensive underwriting.

How much cash can I actually get?

The amount of cash you can receive depends on your homes appraised value, your current mortgage balance, closing costs, and the VA Funding Fee. While you can finance up to 100 percent of the homes value, the actual cash in hand is the appraised value minus your current loan payoff, minus closing costs, and minus the funding fee (if rolled into the loan).

Will my property taxes go up if I refinance?

Generally, refinancing your mortgage does not trigger a reassessment of your property taxes. Property taxes are typically reassessed when a home is sold or when major permitted structural additions are made. A simple refinance transaction should not affect your local property tax bill.

Can I do a VA Cash Out Refinance twice?

Yes, there is no limit to the number of times you can use your VA loan benefit or process a VA Cash Out Refinance, provided you have sufficient equity in your home and meet the income and credit requirements at the time of the new application. Keep in mind that subsequent uses of the VA loan benefit do carry a higher VA Funding Fee (3.3 percent) unless you are exempt due to a service-connected disability.

What are the VA Minimum Property Requirements (MPRs)?

During the appraisal process, the VA appraiser will check the home to ensure it is safe, sound, and sanitary. Common MPR issues include peeling lead-based paint, exposed wiring, missing handrails on stairs, roof leaks, or lack of a functional heating system. If the appraiser flags an MPR issue, it must be repaired before the VA Cash Out Refinance can close.

Important Considerations for Texas Homeowners

If your primary residence is located in the state of Texas, there are unique state laws governing cash out refinances, often referred to as Texas 50(a)(6) loans. Texas law restricts all cash out refinances, including VA loans, to a maximum of 80 percent Loan-to-Value (LTV). This means Texas veterans cannot utilize the 100 percent LTV feature of the VA Cash Out program. If you are a Texas resident, our team at United States VA Loans is fully versed in these specific regulations and will guide you accordingly.

Take Control of Your Financial Future Today

Your home is likely your most valuable financial asset. The equity you have built up over the years represents security, opportunity, and financial freedom. By utilizing a VA Cash Out Refinance, you can unlock that equity to pay off stressful high-interest debt, upgrade your living space, or secure your familys future.

However, refinancing is a major financial decision that requires expert guidance. You deserve to work with a team that respects your service, understands the intricacies of the VA loan program, and puts your financial well-being first.

At United States VA Loans, we are proud to be that team. We are committed to making the refinance process as smooth, transparent, and rewarding as possible.

Contact Danny Plattner and the United States VA Loans Team

Do not leave your home equity sitting idle if it could be working to improve your life. Get the facts, understand your numbers, and make an empowered decision.

Ready to get started?

- Call Us Directly: Reach out to Danny Plattner at 5202411428 for an immediate consultation.

- Email Us: Send your questions or request a callback at unitedstatesvaloans@gmail.com.

- Visit Our Website: Learn more about our services and apply online at www.UnitedStatesVAloans.com.

United States VA Loans is an equal housing lender. All loans are subject to underwriter approval, credit verification, and property appraisal. Interest rates and loan programs are subject to change without notice. The Department of Veterans Affairs does not make loans directly; they guarantee loans made by approved private lenders like us. Contact us today to verify your eligibility and see how much you can save.